Try it now!

Managing your investments has never been easier!

As we approach 2026, the global economy faces a challenging yet potentially transformative year. Leading investment banks across Wall Street and major financial centers project modest growth amid persistent trade tensions and evolving geopolitical landscapes. Central to their optimistic outlook is the role of artificial intelligence (AI), anticipated to significantly enhance productivity and invigorate economic resilience worldwide.

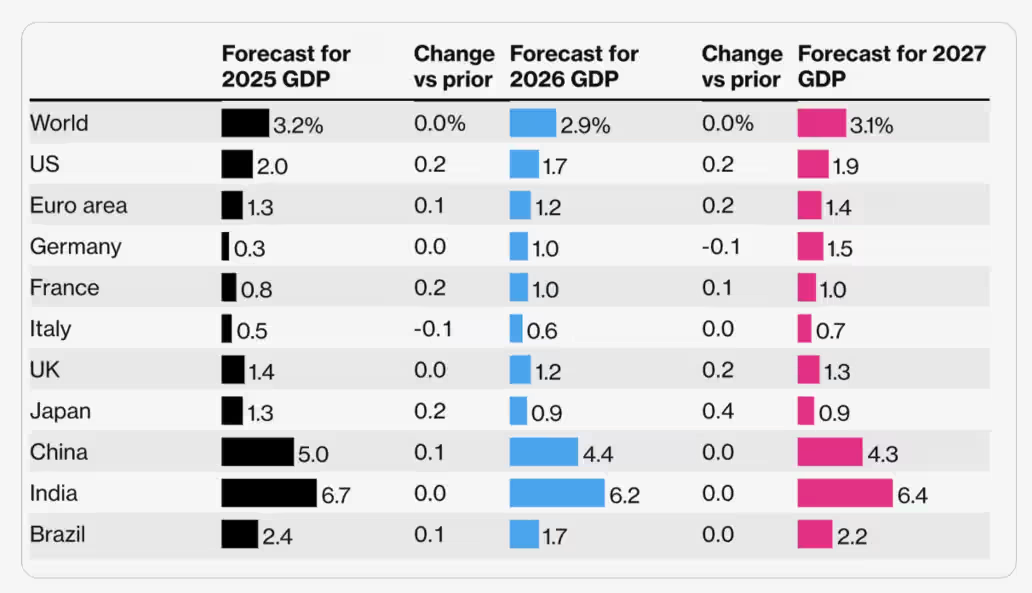

Following a turbulent 2025 marked by heightened tariff disputes and geopolitical uncertainty, the global economic environment is forecasted to slow further in 2026. The Organization for Economic Co-operation and Development (OECD) estimates global GDP growth will decline slightly from 3.2% in 2025 to approximately 2.9% in 2026, reflecting continued adverse effects from trade conflicts and policy uncertainties.

All major economic regions are expected to experience decelerated expansion due to these headwinds. Increased tariffs contribute to elevated inflation, dampened consumer spending, and restrained corporate investments. Nevertheless, major global banks agree that AI's rapid adoption presents a critical counterbalance that could reshape growth trajectories.

US recession fears peaked around the initiation of tariff escalations in 2025 but have noticeably abated. Deutsche Bank's recent survey indicates recession probabilities below 50% among global investors for the year ahead.

The Federal Reserve's interest rate cuts in 2025 and anticipated further easing in 2026 aim to support a steady GDP growth of around 2%. Tax incentives and easing trade policies, combined with substantial corporate investments in AI infrastructure, are expected to underpin this moderate expansion. However, employment gains may remain subdued because AI-related investments often create fewer jobs relative to traditional sectors, introducing political complexities ahead of the 2026 elections.

Political and Market Risks: Intensified scrutiny of Fed independence and potential leadership changes could yield currency volatility and weigh on investor confidence in FX markets.

Europe achieved slightly better-than-expected GDP growth of 1.3% across the eurozone in 2025. However, the 2026 forecast was trimmed marginally to 1.2%, reflecting ongoing international uncertainties and tariff impacts.

US tariffs on EU imports, finalized at 15%, exceed prior expectations and present notable challenges. Inflation is forecast to approach the European Central Bank's 2% target due to offsetting energy and service price trends. Unemployment rates are expected to gradually decline to around 6.2% in 2026.

Germany’s investment package approximating €1 trillion for civilian and defense projects is a key economic driver, signaling a pivot toward enhanced fiscal support.

The Bank of Japan raised rates to a 30-year high in late 2025, responding to slowly improving inflation prospects after a prolonged period near zero rates. The economy saw a surprise contraction in Q3 2025 due to export weaknesses impacted by US tariffs, along with reduced domestic demand pressures.

Despite structural challenges, Japan remains a global provider of low-cost capital, with robust digitalization and automation investments. Monetary policy is expected to continue cautious normalization, with rates potentially reaching 1% by end-2026.

China aims to sustain approximately 4.7% GDP growth in 2026 driven by technological modernization and industrial upgrades rather than large stimulus. After a surprisingly strong 2025 spurred by record export surpluses, policymakers emphasize internal demand growth and high-tech sector advancement, including AI and robotics.

Trade conflicts and a fragile real estate sector remain key vulnerabilities, alongside challenges of aging demographics and overcapacity.

Artificial intelligence emerges as the pivotal megatrend shaping 2026’s economic outlook. Its impact spans productivity enhancement in developed markets to undergirding China’s technological transformation. The AI investment cycle echoes past major capital expansions, positioning it as a significant driver of future growth.

Despite this promise, lingering risks include persistent inflation dynamics, geopolitical instability, labor market shifts, and regulatory challenges across regions.

Investor Considerations: Monitoring AI integration across sectors, evaluating geopolitical risks, and staying agile amid changing monetary policies will be essential for capitalizing on emerging opportunities.

Investors seeking detailed, data-driven strategic insights can explore personalized recommendations with 8FIGURES, the AI-powered investment advisor designed to navigate complex financial markets confidently.

Managing your investments has never been easier!