Try it now!

Managing your investments has never been easier!

For the past 15 years, U.S. stocks have been the undisputed global champions. Powered by mega-cap tech giants, the S&P 500 has consistently outperformed nearly every major market in the world. But looking forward, investors shouldn't assume the next decade will resemble the last.

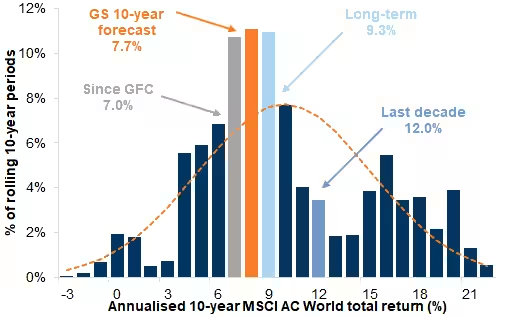

A detailed long-term outlook from Goldman Sachs' global strategy team suggests that U.S. stocks may deliver the lowest returns among major equity regions over the next 10 years, not because America's economy is weak, but because valuations have become elevated relative to the rest of the world.1

Here's what long-horizon investors need to know, region by region, about potential stock market returns and investment opportunities.

Despite high valuations in many markets, Goldman expects global stocks to return about 7.5%–8% annually (in USD) over the next decade.1 That's slightly below historical norms but comfortably positive. The biggest engine of returns worldwide remains the same as always:

Corporate profitability, boosted by buybacks, is expected to remain resilient globally, with company earnings driving much of the total return.

Most regions will generate 2–3% yields.

Today's elevated earnings multiples are likely to drift lower, trimming 0.5%–1% per year from returns.

Importantly, Goldman's baseline does not assume a recession, systemic financial crisis, or an artificial intelligence-driven productivity boom.1 Instead, it models a world of modest inflation (~2%), stable interest rates, and steady, if unspectacular, GDP growth.6

There are alternative paths:

For U.S. investors, the headline number may be surprising:

Expected S&P 500 return (next 10 years): ~6.5% per year.1 Roughly 4.3% real return after inflation.

That's not bad, just lower than the market has delivered since the 2010s.

Forward P/E ratios near 23x are well above historical averages. Even if earnings continue to grow, Goldman expects multiples to drift down toward ~21x by 2035.2 This high PEG ratio suggests caution for value-oriented investors.

U.S. corporations have enjoyed a decades-long rise in:

But many of the forces behind the margin boom, globalized supply chains, falling corporate tax rates, lower interest costs are unlikely to repeat.

Goldman does not explicitly price in large artificial intelligence productivity gains, but notes they could:

Conversely, margin compression in tech, the sector that carried markets for a decade, is the biggest risk to U.S. stock market returns.

Europe's equity markets get far less attention from American investors, but they may offer competitive returns going forward.

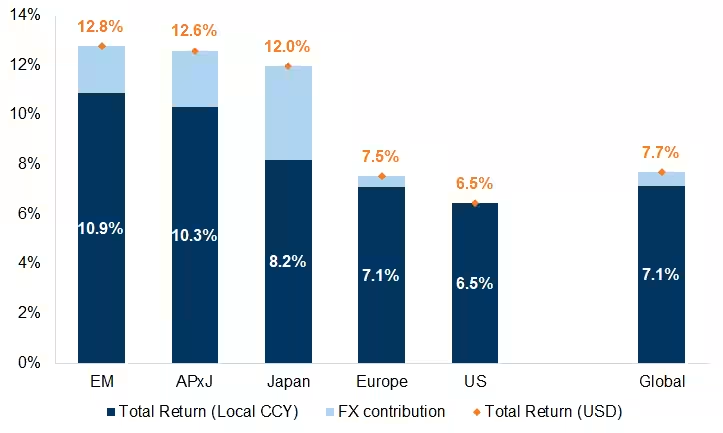

Expected European equity return: ~7% in EUR (~7.5% in USD)1

Europe's outlook is the most "balanced" in Goldman's framework: real upside if market integration and productivity improve, real downside if the region slips back to slow pre-pandemic growth.

Asia-Pacific markets (excluding Japan) show the greatest divergence, some of the strongest earnings expectations alongside significant geopolitical risks and trade tensions.

Baseline return for MSCI Asia ex-Japan: high single digits in USD, potentially boosted by emerging market currency appreciation.

Asia stands to benefit from:

Goldman also expects a broadly weaker U.S. dollar, which could add 2–3% annually to USD returns in Asian equities, benefiting emerging market currencies.

The biggest headline in the forecast:

Expected emerging market equity returns: ~12–13% annually in USD*(Significantly above both the U.S. and developed markets.)1

Still, relative to the U.S., the return premium for emerging markets stocks is striking. The MSCI Emerging Markets Index and EM equities broadly could see significant outperformance.

The four regions this article examines differ less in raw opportunity than in valuation starting points, what is driving corporate profits, and what could go wrong.

| Region | Valuation Stance | Key Growth Drivers | Key Risks |

|---|---|---|---|

| United States | Forward P/E near 23x, well above historical norms; Goldman expects multiples to drift toward ~21x by 2035 | Exceptional profitability — net margins, return on equity, global market share, and buybacks | Margin compression in the tech sector that carried the market for a decade; tailwinds (globalized supply chains, falling tax rates, lower rates) unlikely to repeat |

| Europe | Forward P/E around 14–15x — more reasonable than the U.S.; dividend yield ~3% | Global revenue base — only 40% of sales come from Europe itself — plus dividend income | Political cohesion within the EU, pace of green-energy investment, and recovery of manufacturing competitiveness are open questions |

| Asia ex-Japan | Wide dispersion across markets rather than one regional multiple; earnings expectations vary sharply by country | Chip production, data-center buildouts, and supply-chain diversification — led by India, Taiwan, South Korea, ASEAN, and China, plus governance reforms in Korea, Japan, and Taiwan | Significant geopolitical risk and trade tensions alongside the strongest earnings expectations of the four regions |

| Emerging Markets | Expected P/E around 12.8x a decade from now — the most attractive valuation of the four regions | Faster GDP growth than the U.S., stronger expected earnings growth, and a historically favorable weaker-dollar tailwind | Policy unpredictability (e.g., China, parts of LATAM), commodity dependence (Brazil, South Africa), and governance/capital-inflow volatility |

As of the November 12, 2025 Goldman Sachs Global Investment Research regional equity outlook cited above. Valuation and driver figures are Goldman’s current framework, not a guarantee of future results — markets can and do deviate from any published outlook. Use the 8FIGURES Portfolio Analyzer to see how your own global allocation lines up against these regional weights.

U.S. stocks may continue to outperform—but the margin of advantage is shrinking. Global equity funds offer exposure to a wider range of investment opportunities.

But they come with the highest stock market volatility. Dollar weakness could be a powerful tailwind for emerging market currencies and overall performance.

Dividends and moderate valuations support mid-single-digit real returns, with potential upside from market integration efforts.

From India's demographic advantages to Taiwan's semiconductor dominance, the region is a long-term growth engine for emerging market equities.

If productivity gains materialize globally—not just in U.S. tech—the next decade could surprise to the upside, potentially sparking an innovation boom across financial markets.

U.S. stocks will likely remain among the world's most innovative and profitable, but high valuations may cap their future returns. Investors with long horizons should consider increasing exposure to regions where structural growth, demographics, and valuations are more favorable: emerging markets, Asia, and parts of Europe.

The MSCI EM Index and emerging market funds could be particularly attractive for those seeking higher potential returns and willing to accept increased volatility. Emerging market outperformance may be driven by a combination of economic fundamentals, favorable demographics, and currency tailwinds.

As always, long-term asset allocation, not short-term market timing, will be the biggest driver of success over the next decade. Investors should carefully consider their risk tolerance, monitor geopolitical risks, and stay attuned to shifts in monetary policy and interest rates that could impact both developed and emerging market equities. To make these decisions easier and more data-driven, you can turn to the 8FIGURES AI Investment Advisor, which helps identify opportunities, assess risks, and build globally diversified portfolios aligned with long-term goals.

REFERENCES

Managing your investments has never been easier!