.avif)

Try it now!

Managing your investments has never been easier!

The Federal Reserve is expected to keep policy rates elevated until at least mid-2025 and cut only gradually thereafter, according to futures pricing and a May Reuters poll of economists. That leaves short-term Treasuries yielding just 4–4.5%, while equity markets remain choppy. Real estate investment trusts (REITs), a popular form of real estate stocks, must distribute at least 90% of their taxable income, so—when chosen carefully—they can still deliver double-digit cash yields without locking investors into long-duration bonds. This makes REITs an attractive option for those seeking the best real estate stocks in the current market environment.

Below are three of the best REITs to invest in that operate in very different corners of the mortgage and commercial real estate landscape yet currently pay some of the richest dividends available on U.S. exchanges. These high dividend REITs demonstrate why REIT investing can be an attractive option for income-seeking investors in the stock market. Each profile explains how the dividend is funded, what could make it grow, and what could put it at risk, helping you understand the potential REIT returns and risks associated with these top 10 REIT stocks.

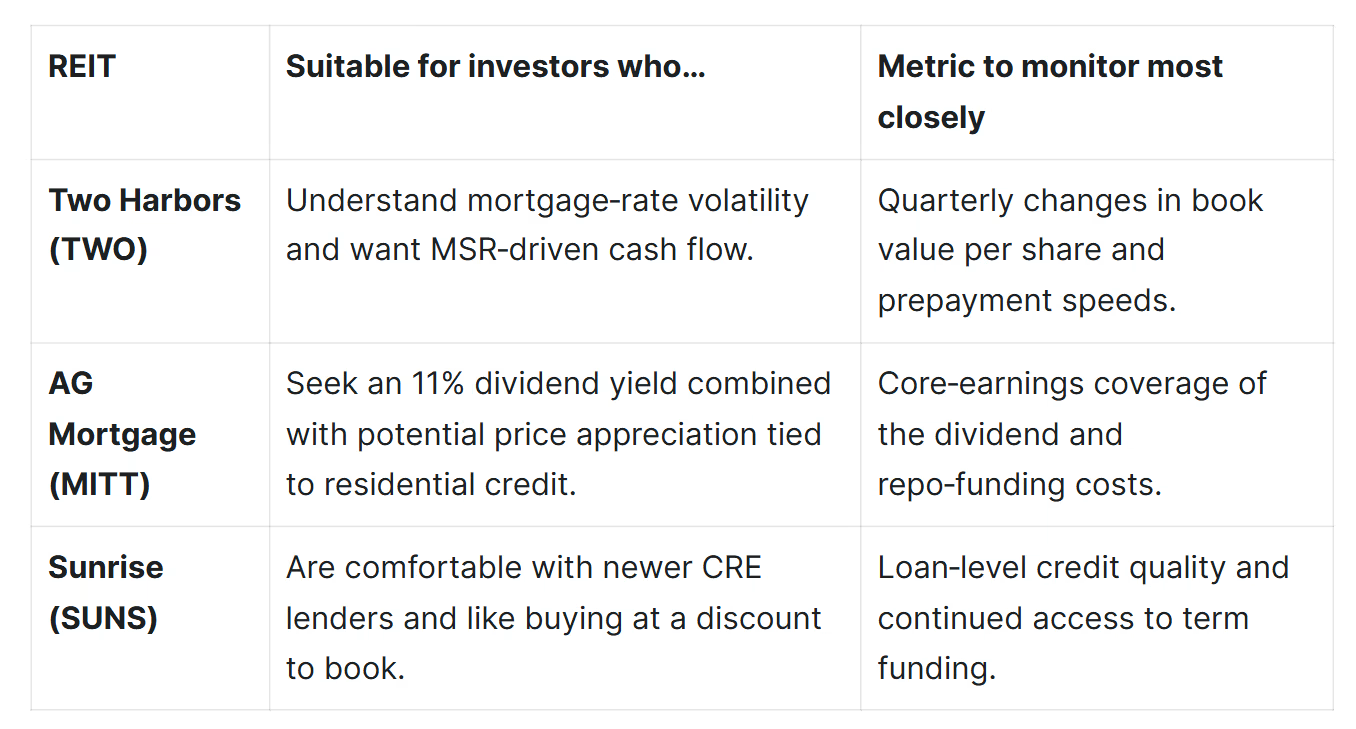

Two Harbors, an equity REIT, earns fee income by owning mortgage‑servicing rights (MSRs) on conforming loans through its RoundPoint platform. It hedges the associated interest‑rate and prepayment risk with a mix of agency and non‑agency mortgage‑backed securities (MBS). At the end of the first quarter of 2025 the company reported book value of $14.66 per share and produced a 4.4% economic return for the quarter.

The company paid a quarterly dividend of $0.45 per share on 29 April 2025. At a share price of roughly $11.80, that payout translates into a forward dividend yield of about 15%. Management continues to repurchase shares when they trade below book value, which provides an additional layer of support for per‑share results. This high yield makes Two Harbors one of the best dividend REITs in the market, offering attractive rental income potential for investors.

AG Mortgage Investment Trust buys newly originated, higher‑credit‑quality residential loans, funds them on repo or warehouse lines, and then packages the loans into non‑recourse securitisations using affiliate TPG Angelo Gordon's platform. The investment portfolio stood at $7.1 billion on 31 March 2025.

In March 2025 the board raised the quarterly dividend to $0.20 per share, an increase of 5.3%. At a share price near $7.15, the forward dividend yield works out to roughly 11%. The most recent payout consumed 89% of trailing GAAP earnings, and management has signalled a long‑term target in the mid‑80% area when measured against core earnings. This consistent dividend growth makes AG Mortgage Investment Trust one of the best REIT dividend stocks for income-focused investors.

The Wall‑Street consensus projects earnings per share of about $0.94 for 2025 and $1.07 for 2026. Analysts' average price target sits around $8.25, implying 15–20% potential upside on top of the dividend. As mortgage rates drift lower, MITT expects securitisation volumes and gain‑on‑sale margins to improve.

Formed in 2023 and headquartered in West Palm Beach, Florida, Sunrise originates senior and mezzanine loans on transitional projects in high‑growth Southern markets. With many regional banks scaling back commercial property exposure, Sunrise is able to command unusually wide credit spreads on its loans.

For the first quarter of 2025 the company paid a dividend of $0.30 per share on 15 April 2025. Based on a share price that has recently traded between $10 and $11, the forward dividend yield ranges from 10% to 11%. Sunrise generated distributable earnings of $0.31 per share in the same quarter, comfortably covering the payout. While not among the REITs that pay monthly dividends, Sunrise's attractive quarterly yield makes it a compelling option for income investors.

In the May investor presentation, management said they can grow the loan portfolio by roughly 40 % in 2025 without over-leveraging the balance sheet and still generate at least $0.30 per share of distributable earnings in Q2. The stock trades at about 70 % of its book value, so if management meets these targets and the market recognizes the progress, the share price could move closer to book. That blend of steady income and potential price upside makes Sunrise an attractive growth-oriented REIT pick.

If the Federal Reserve begins easing policy this summer, lower short‑term funding costs should benefit all three trusts. Nevertheless, falling long‑bond yields can be a double‑edged sword: they boost MSR values (which helps Two Harbors) yet compress net‑interest spreads and accelerate mortgage prepayments (which challenges both Two Harbors and MITT). For Sunrise, the bigger swing factor is the health of the commercial real estate market; even if rates fall, a recession would still pose credit‑loss risk. This interest rate sensitivity is a crucial factor to consider when investing in REITs.

When considering how to invest in REITs, remember that these investments offer potential benefits such as income generation, diversification, and exposure to property ownership without direct management responsibilities. REITs also provide tax advantages, as they are required to distribute most of their taxable income to shareholders. However, they also come with risks, including interest rate sensitivity and market volatility.

While these top performing REITs offer attractive dividend yields, it's essential to conduct thorough research and consider your investment goals before adding them to your portfolio.

At 8FIGURES, we strip out the guesswork so your high-yield ideas don’t become high-risk surprises. Our AI Portfolio Analyst digs into each trust’s drivers—book-value trends, funding costs, rate sensitivity—and blends that detail with your goals and risk limits.

Managing your investments has never been easier!