.avif "Growth Investing: Finding High-Potential Companies")

Try it now!

Managing your investments has never been easier!

When Nvidia reports, the entire market listens. Its chips power the artificial intelligence revolution, from training foundation models to running massive data centers, and its results increasingly act as a sentiment gauge for the entire tech sector.

This quarter's numbers carried even more weight than usual. For weeks, investors debated whether AI spending is hitting unsustainable extremes. Bank of America's latest fund manager survey showed 45% of respondents calling an "AI bubble" the biggest risk to markets, up sharply since the fall.

Against that backdrop, Nvidia delivered an earnings call so widely anticipated that The Wall Street Journal dubbed it "the financial Super Bowl."

After reviewing Nvidia's earnings and several post-report notes from top Wall Street analysts, here's what matters most, and what it means for the U.S. market.

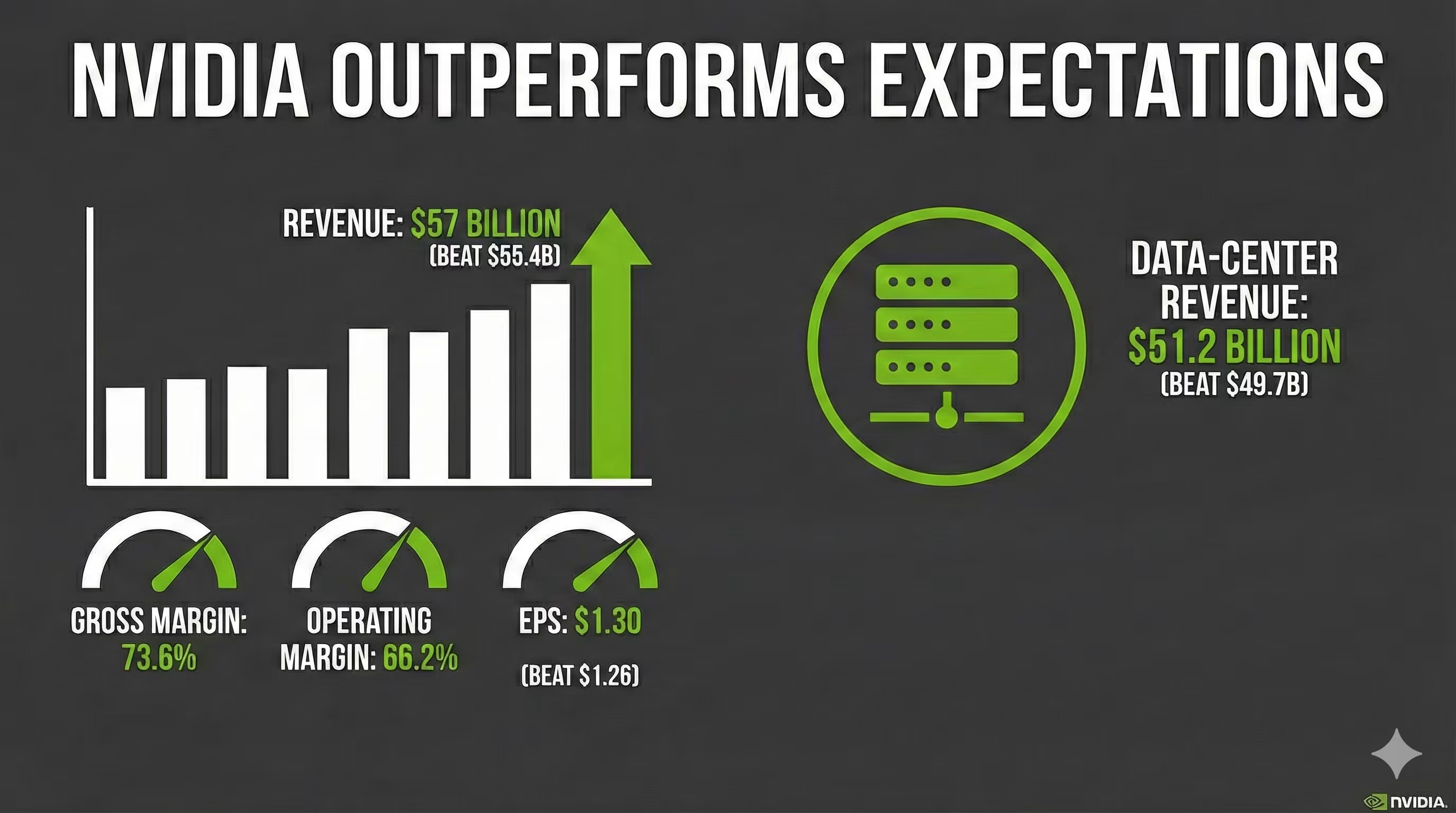

Despite already-lofty expectations, Nvidia outperformed across nearly every major line item:

Gaming and automotive came in slightly soft, but those categories are now rounding errors compared to the data-center juggernaut.

The core story remains the same: hyperscaler companies are still buying every AI accelerator Nvidia can produce.

Nvidia's data-center segment grew 56% year-over-year, powered by demand from hyperscaler companies like Meta, Microsoft, Oracle, and the rapidly scaling xAI.

Management reiterated, more confidently than before, that demand for its Blackwell AI chips and Rubin product families could surpass $500 billion between 2025 and 2026.

Nvidia also reaffirmed a massive long-term estimate: global spending on AI infrastructure could reach $3–4 trillion per year by 2030, driving significant cloud computing spend.

A striking detail from the earnings call: many Ampere-generation GPUs (launched up to six years ago) are still running at or near full utilization inside customer clusters.

For investors, this signals:

Customers are increasingly choosing Nvidia's highest-performance chips, supporting margins even as component costs rise.

Nvidia's outlook for the upcoming quarter was the real shock:

This implies 10× revenue growth in just three years.

Bloomberg noted that despite recent fears of overspending on accelerators, Nvidia sees no slowdown in demand. CEO Jensen Huang emphasized artificial intelligence's continued integration into search, enterprise workloads, automation, and soon robotics, the next frontier.

A controversial topic on Wall Street: Nvidia's strategic investments in major AI customers such as OpenAI and Anthropic.

Critics worry these deals create circular AI deals:

This quarter, Huang directly addressed the issue:

For now, analysts view these relationships as strategic, not merely financial engineering through special purpose vehicles.

Even as demand rises, Nvidia's biggest challenge is meeting it.

Constraints include:

Morgan Stanley noted last week that growth will require "dynamic supply-chain management" and more willingness to secure long-lead commitments with suppliers.

Still, Nvidia's Q4 data-center forecast suggests bottlenecks are easing enough to support massive year-end shipments.

Following the report, semiconductor stocks globally surged:

Yet U.S. markets didn't hold their early gains.

By the close:

Why the selloff? Several reasons:

Goldman Sachs raised its Nvidia EPS estimates by 12% on average and initiated long-term forecasts through 2030.

The bank now sees:

Goldman maintains a Buy rating with a new price target of $250, based on:

Current stock price: ~$187.

Consensus among analysts:

Goldman highlights several key risks:

If hyperscaler companies curb capex, demand could normalize quickly.

AMD, Broadcom, and Qualcomm are now more vocal about gaining share.AMD projects 80% CAGR in AI chip sales and sees potential for a double-digit market share by 2030.

Cloud providers are also doubling down on custom silicon to reduce reliance on Nvidia.

More competition could force price concessions.

U.S. export controls have effectively cut Nvidia off from China's AI-accelerator market. Huang says the company currently assumes zero China sales in its forecasts. Still, the U.S. Commerce Department recently approved shipments of advanced AI chips to government-backed firms in the UAE and Saudi Arabia—signaling a more flexible stance going forward.

Nvidia's report temporarily eased fears of an artificial intelligence bubble, but hasn't eliminated them.

Nvidia’s quarter didn’t settle the AI-bubble question — it sharpened both sides of it, as the numbers below from the same earnings cycle show.

| Dimension | Bull Case | Bear Case |

|---|---|---|

| Demand vs. infrastructure buildout | AI is framed as a multi-trillion-dollar infrastructure cycle with demand still running above supply; data-center revenue grew 56% year-over-year and management sees Blackwell/Rubin chip demand topping $500B between 2025 and 2026. | Capex cycles can turn abruptly if hyperscaler ROI disappoints, and slower AI infrastructure spending is flagged as a top risk to the current growth trajectory. |

| Competitive position & margins | Nvidia holds dominant market share with unmatched developer tools and pricing power; even six-year-old Ampere GPUs are still running near full utilization in customer clusters, a sign compute demand isn’t overbuilt. | Rising competition from AMD, Broadcom, and Qualcomm, plus cloud providers building custom silicon, could pressure Nvidia’s margins over time. |

| Macro & valuation backdrop | Sell-side sentiment stayed broadly positive after the print, with analysts pointing to continued data-center demand. | Valuations across AI equities remain stretched, and the S&P 500 (–1.6%) and Nasdaq-100 (–2.4%) both sold off the same day on Fed-policy and macro uncertainty — even as semiconductor stocks rallied. |

As of Nvidia’s Q3 FY2026 earnings report, November 24–25, 2025. Bull/bear framing and figures per the article above and Goldman Sachs’ November 2025 “AI: In a Bubble?” research note; single-day price moves are not indicative of future performance. For ongoing exposure tracking across AI and semiconductor holdings, the 8FIGURES stock tracker can help investors monitor concentration in high-beta names like these as the debate develops.

The fundamental debate remains:In short, Nvidia may have bought the market some breathing room, but investors are still wrestling with the bigger question:

Is this truly the start of a decades-long artificial intelligence supercycle, or simply the hottest phase of a boom that will eventually cool?

As of now, the numbers strongly favor the bull case.But the volatility around this earnings call shows one thing clearly: AI stocks will remain a high-beta trade for the foreseeable future.

For investors trying to navigate this landscape, the 8FIGURES AI Investment Advisor helps cut through the noise by assessing portfolio risk, measuring exposure to high-beta AI stocks, and evaluating the sustainability of earnings expectations across the semiconductor supply chain.

REFERENCES:

Managing your investments has never been easier!