Try it now!

Managing your investments has never been easier!

As Wall Street kicks off its earnings season, investment banks are commanding attention as beneficiaries of a revitalized capital markets environment. Market leaders like Goldman Sachs underscore the sector’s exceptional growth prospects driven by surging mergers and acquisitions (M&A), increased equity and debt issuances, and renewed investor appetite. Here, we explore the bullish rationale behind this trend and spotlight three top-tier investment banks poised to capitalize on the momentum.

Investment banks delivered remarkable performances in 2025, marking their best showing since 2021. The leading five U.S. banks generated a record-breaking $134 billion from trading activities, a 15% year-over-year rise. The six largest institutions, including JPMorgan Chase and Citigroup, posted their highest profits since 2021, fueling optimism as the earnings season unfolds.

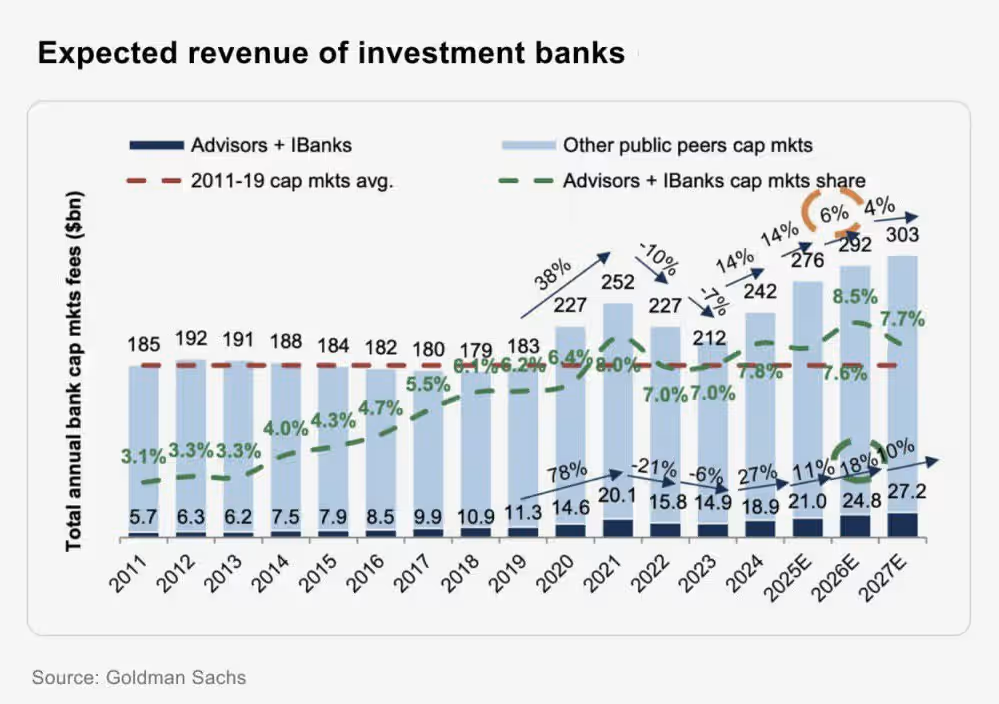

According to Goldman Sachs, client demand for advisory, debt, and equity capital raising services has reached multi-year highs, underpinning stronger bank earnings and outlooks. Goldman Sachs projects average annual revenue growth for investment banks at 13% from 2025 through 2027, eclipsing the 9% growth anticipated in 2025 alone. Earnings per share (EPS) growth is forecasted to surge at a compound annual growth rate (CAGR) of 27% over that period.

The M&A market is currently in early to mid-cycle recovery. After volumes fell by roughly 50% between 2021 and 2023, they rebounded by 11% in 2024 and surged 45% in 2025. Goldman Sachs anticipates continued growth with an estimated 21% advance in 2026. Historically, M&A cycles exhibit growth of about 155% to 165% over 4 to 5 years from bottom to peak, indicating this recovery phase is approximately halfway through its trajectory.

Despite these gains, announced deals remain near historical lows relative to global market capitalization, sitting around 5–6% compared to a long-term average closer to 10%. This gap signifies a strong pent-up demand for corporate restructuring, consolidation, and portfolio optimization.

The equity capital markets (ECM) sector faced a severe contraction between 2021 and 2023, shrinking by approximately 65%. The market rebounded with a 22% rise in 2024 and a further 20% increase in 2025, with expectations of accelerating activity in 2026. Crucially, IPOs from private equity-backed companies are pivotal to this revival, enabling funds to return capital and ignite additional waves of corporate transactions.

Investment banks derive about two-thirds of their revenues from M&A advisory and capital-raising services. Other business segments, such as restructuring and trading—which helped banks weather downturns—are expected to grow at a slower pace as cyclical markets normalize.

Despite the sector’s improving fundamentals in 2025, stock prices of investment banks showed modest gains. Future stock appreciation will likely rely more on earnings growth rather than expansion of valuation multiples, which currently sit near the 85th to 90th percentile relative to historical price-to-earnings (P/E) ratios over the past decade.

Goldman Sachs holds a cautiously optimistic stance on near-term EPS relative to consensus estimates and foresees diminishing gaps between investor expectations and earnings by 2027, fueled by the capital markets revival.

Founded in 1995 by former U.S. Deputy Treasury Secretary Roger Altman, Evercore stands out as one of the largest independent advisory firms on Wall Street, focusing solely on strategic advisory and capital markets services without lending or retail banking distractions.

Financially, Evercore posted record Q3 2025 revenue of $1 billion, up 41% year-over-year, and $2.6 billion for the first nine months, a 28% increase. Operating profit soared 77% to $216 million, pushing margins to 20.8%. Higher personnel costs, driven by bonuses and hiring, rose 39% in Q3 but were offset by strong revenue growth, resulting in a lowered compensation ratio of 65.5%.

Evercore demonstrates shareholder-friendly capital deployment via quarterly dividends of $0.84 per share and year-to-date share buybacks totaling 1.9 million shares. Its high-margin, capital-light model and improving deal flow underpin an attractive valuation.

Founded in 1972, Houlihan Lokey is a global leader in advisory services, excelling in M&A, capital raising, and financial restructuring, primarily targeting middle-market companies across healthcare, technology, financial services, and industrial sectors.

In Q2, the firm reported $659 million in revenue and $112 million in net income, reflecting sustained momentum. CEO Scott Adelson expressed confidence in ongoing growth through the rest of 2026. Personnel costs rose moderately, slightly increasing the compensation ratio to 64.2%, while operating margins remained near 30%.

Goldman Sachs rates Houlihan Lokey as a Buy, listing it on their Americas Conviction List with a 12-month price target of $237, implying 36% upside. The investment thesis emphasizes diverse revenue streams, secular growth, and a blend of organic and acquisition-driven expansion.

Piper Sandler operates a diversified boutique model catering primarily to U.S. clients with advisory, brokerage, and trading services. Its expertise spans financial services, healthcare, technology, and municipal bonds, with offices in the U.S., U.K., EU, and Hong Kong.

Net revenues for Q3 were $479.3 million, a sequential 21% and annual 33% increase. CEO Chad Abraham highlighted robust client engagement and a positive outlook to close 2025 strongly.

The firm completed 82 deals in Q3, up 15% year-over-year, focusing on M&A and restructurings with a sharp uptick in capital raises. Municipal bond issuance volume grew, despite a small decline in transaction count post a strong Q2.

Piper Sandler improved cost discipline, benefiting from revenue leverage and a reduced effective tax rate, which supported net earnings. The company pays a $0.70 quarterly dividend (approximately a 1.54% yield) and repurchased 362,000 shares year-to-date.

Goldman Sachs rates Piper Sandler as a Buy with a $418 price target, indicating 23% potential upside. Its diversified business, strong M&A backlog (up nearly 140% since early 2024), and potential benefits from rate cuts and deregulation support an expected 11% revenue CAGR through 2027.

Investment banks are entering a prime phase fueled by vibrant M&A activity, IPO resurgence, and sustained capital markets expansion. Selecting high-quality players positioned to benefit from these trends offers investors compelling opportunities in the financial services landscape.

For personalized guidance and to explore cutting-edge investment strategies in financial sectors and beyond, use 8FIGURES, the AI Investment Advisor devoted to helping investors navigate complex markets with confidence.

Managing your investments has never been easier!