.avif "Value Investing: Finding Undervalued Stocks & Growth")

Try it now!

Managing your investments has never been easier!

Amid fading political uncertainties and emerging signs of a productivity resurgence, the UK stock market appears well-positioned to sustain and build on the robust gains achieved in 2025. Investors seeking strategic diversification should closely consider Britain’s evolving economic landscape and the promising investment opportunities it offers for 2026.

In early February 2026, UK Prime Minister Keir Starmer faced significant political pressure related to the fallout from the Jeffrey Epstein files, including calls from within his own party for him to resign after controversy over the appointment of Peter Mandelson, a former ambassador linked to the scandal. Despite this turmoil and the resignation of key aides, he remained in office as rival figures stopped short of forcing a leadership challenge. This easing of political uncertainty may help maintain investor confidence following the British equity market’s strong returns in 2025.

The United Kingdom has struggled with a longstanding "productivity puzzle" since 2010, where official forecasts of labor productivity growth repeatedly failed to materialize, hampering economic expansion. This has hampered growth and kept the Bank of England’s policy rates elevated for years.

Recent data, however, suggest that this narrative is shifting. Companies are increasing capital expenditures while hiring cautiously, signaling improving output per worker. According to economist Dean Turner from UBS Wealth Management: “If firms produce more without increasing headcount, productivity is the only explanation.”

Official figures report a modest 2.3% rise in UK labor productivity since 2019, but alternative metrics based on payroll tax data indicate a stronger 3.7% increase over the same period, including a notable 3.1% jump last year. This suggests that productivity growth may be underrepresented in official statistics yet is gaining momentum in the real economy.

Why productivity matters: Productivity growth dictates sustainable economic expansion without triggering inflation. The Bank of England’s forecast of an acceleration to 1% annual productivity growth could pave the way for looser monetary policy and better market conditions.

Several indicators corroborate the narrative of a UK economic revival:

This revival is underpinned by key structural shifts:

Both public and private sector investment in the UK is rising after a period of underinvestment that weighed on productivity. The government plans to increase public sector gross investment to more than £180 billion ($247 billion) by 2030–31, about 25% higher than in 2024–25.

Private capital is also mobilizing, driven by tax incentives and investments in the energy transition and digital transformation. Capital expenditures jumped 9% over the past two years, reversing Brexit-related slowdowns and positioning firms for higher efficiency.

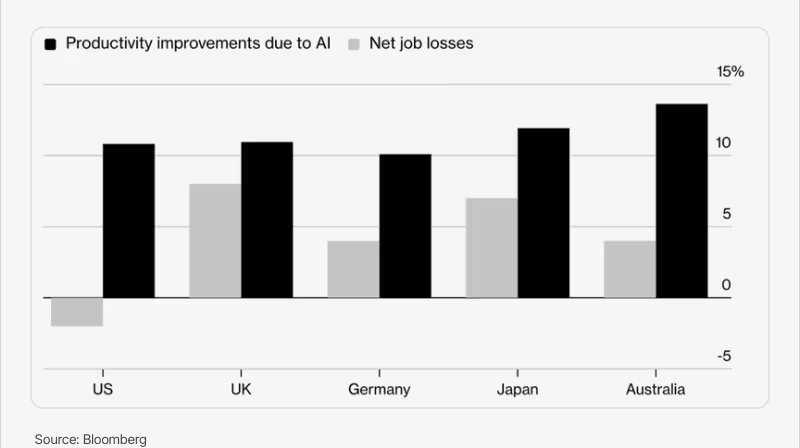

Morgan Stanley estimates AI's productivity boost could raise company output by 0.6% annually over the next three years. The Bank of England's surveys underscore AI as a crucial factor revitalizing productivity, reminiscent of the momentum seen during the internet and computer revolutions.

Although skepticism around the UK economy has persisted for years, the FTSE All-Share Index—which represents nearly all companies listed on the London Stock Exchange, delivered a strong performance in 2025, rising close to 19%. That marked one of its best annual gains since 2009. By comparison, the global MSCI All Country World Index (ACWI) advanced roughly 21% over the same period.

Looking ahead to 2026, some market strategists believe the UK stock market could extend its momentum, particularly if the Bank of England continues cutting interest rates. According to Bloomberg, improving investor sentiment toward Britain reflects both easing macroeconomic concerns and the resilience and competitiveness of UK-listed companies.

Among the most notable performers in 2025:

LSEG transformed into a diversified financial market infrastructure and data provider after acquiring Refinitiv in 2021, shifting revenue towards steadier, recurring streams from data and analytics platforms.

The company operates four main segments: Data & Analytics, FTSE Russell Indices, Risk & Compliance, and Market Infrastructure.

Activist investor Elliott Management recently took a stake, pushing for operational improvements amid slowing growth in the lucrative Data & Analytics segment, which constitutes nearly 45% of revenue.

Goldman Sachs estimates AI poses under 6% direct revenue risk to LSEG, and the company is actively collaborating with tech leaders like Microsoft and OpenAI to harness AI advances.

LSEG reported 6.9% revenue growth in the first half of 2025, reaching £4.5 billion ($6.1 billion), with rising trading volumes and higher operating margins fueled by cost efficiencies. Net profit improved, supported by a strategy of bond buybacks and capital returns, including a 14.6% interim dividend hike and share buybacks totaling £4 billion ($5.5 billion) since 2022.

8FIGURES Takeaway: Elliott Management’s involvement often unlocks value through improved margins and shareholder returns, positioning LSEG for enhanced profitability and capital distribution.

Melrose Industries focuses on aerospace components for civil (66%) and defense (34%) sectors, serving prime contractors such as Airbus, Boeing, Rolls-Royce, and Pratt & Whitney.

Its two segments are:

Long-term growth drivers include a large civil aviation backlog (approximately 15,000 aircraft orders) and increasing military budgets among NATO allies aiming for 5% of GDP by 2035, which support demand for aircraft and component suppliers.

In H1 2025, Melrose reported £1.72 billion ($2.3 billion) in revenue, stable with 6% underlying growth excluding divestments. Operating profits rebounded strongly to £441 million ($601 million) with margins at a healthy 26.4%, reflecting restructuring success and lower defect rates.

The company improved dividends by 20% and engaged in share repurchases despite negative operating cash flow, anticipating improved cash generation as restructuring benefits take hold.

8FIGURES Takeaway: Melrose offers exposure to robust civil aviation growth and defense spending with predictable revenue streams and attractive valuation metrics.

Haleon, spun off from GlaxoSmithKline in 2022, commands a leading position in consumer health products focusing on six categories: oral care, vitamins, analgesics, respiratory, digestive health, and dermatology.

Brands include Advil, Centrum, Sensodyne, and Otrivin, with recent divestitures sharpening focus on higher-margin and faster-growing segments, especially oral care and analgesics.

Growth factors:

Haleon’s H1 2025 revenue decreased 3.8% to £5.48 billion ($7.5 billion), but organic growth reached 3.2% aided by pricing and volume gains in EMEA, Latin America, and Asia-Pacific. Operating profitability improved with margin expansion through supply chain efficiencies and controlled marketing spending.

Strong cash flows supported a 10% interim dividend increase and £370 million ($504 million) in share buybacks.

8FIGURES Takeaway: With a strong brand portfolio and defensive demand characteristics, Haleon offers steady growth attractive to long-term shareholders.

The convergence of political stability, a long-awaited productivity turnaround, and improving business confidence creates a compelling case for increasing exposure to British equities. Monitoring the productivity recovery will be critical as it signals potential monetary easing and underlying economy strength.

Among UK-listed companies, London Stock Exchange Group’s activist-led transformation, Melrose Industries’ positioning for aerospace and defence growth, and Haleon’s resilient consumer health business stand out as particularly promising investment opportunities supported by durable secular trends.

Managing your investments has never been easier!